Introduction

Calibration gas mixtures are precisely formulated blends used to validate the accuracy of analytical instruments across industrial, environmental, and safety applications. From continuous emission monitoring systems (CEMS) at power plants to multi-gas detectors in confined spaces, these certified reference blends keep measurement equipment compliant and reliable.

For procurement managers, lab directors, and industrial operators, calibration gas is a non-negotiable input — directly tied to regulatory compliance, worker safety, and product quality.

The calibration gas market in 2026 looks meaningfully different from five years ago — and the pace of change is accelerating. Environmental mandates are expanding the list of regulated pollutants. Energy transition technologies are creating demand for new formulations. Semiconductor fab investments are straining ultra-high-purity supply chains.

Geopolitical fragmentation is pushing buyers to rethink supply reliability altogether.

What follows breaks down the specific forces reshaping calibration gas demand in 2026 — so procurement professionals can anticipate supply shifts, identify sourcing risks, and make purchasing decisions before the market moves against them.

Key Takeaways

- The calibration gas mixture market is projected to grow from USD 0.77 billion in 2026 to USD 1.22 billion by 2035, driven by environmental compliance, energy transition investments, and industrial automation

- CEMS demand—now roughly 30% of total calibration gas consumption—is durable and growing as regulated pollutant lists expand

- Hydrogen fuel cells, EV battery testing, and semiconductor gigafactories are driving demand for premium, specialized gas formulations

- Specialty blenders are pulling ahead of commodity suppliers in complex reactive mixtures and ultra-high-purity applications

- Geopolitical risks and ISO 17034 accreditation barriers are tightening custom blend supply—favoring NIST-traceable producers who can move fast

Tightening Environmental Regulations Are Expanding CEMS Demand Globally

Continuous emission monitoring systems (CEMS) have become a mandatory fixture at industrial facilities worldwide. Legislation such as the EU Industrial Emissions Directive, China's Blue Sky Policy, and the US Clean Air Act creates non-discretionary, recurring demand for calibration gas mixtures at industrial stacks, fence-line monitors, and government air quality stations.

Regulatory-Driven Calibration Frequency

Under the US Clean Air Act, 40 CFR Part 75 mandates rigorous quality assurance testing that consumes substantial volumes of certified calibration gas:

- Daily 2-point calibration error tests on every operating day

- Quarterly 3-point linearity checks at defined intervals

- Certified calibration gas concentrations verified to analytical uncertainty ≤ ±2.0% at the 95% confidence interval

This high-frequency calibration requirement creates a predictable, high-volume consumption pattern — fundamentally different from routine industrial gas purchases. Even during economic slowdowns, CEMS operators must maintain calibration compliance, making this demand segment structurally resilient.

Expanding Pollutant Coverage

The regulated pollutant list is expanding beyond traditional criteria pollutants (NOx, SO₂, CO, O₃) to include greenhouse gases such as CH₄ and CO₂. The EU's Regulation (EU) 2024/1787, which entered force in August 2024, sets strict rules to measure, monitor, report, and reduce methane emissions in the energy sector. China launched a national CEMS network for high-emitting sectors and released a Methane Emissions Control Action Plan in late 2023.

Each new regulated parameter requires a certified calibration gas formulation. As both the number of regulated facilities and the scope of regulated pollutants increase, the total volume of calibration gas consumed compounds with each regulatory cycle.

Market Scale

The global emission monitoring systems market was estimated at USD 3.50 billion in 2023 and is projected to reach USD 6.71 billion by 2030, growing at a CAGR of 10.3%, with CEMS holding more than 79% of global revenue. Environmental monitoring accounts for approximately 30% of total calibration gas mixture demand, making it the single largest end-use segment.

Why Regulatory Demand Keeps Growing

New environmental legislation is being enacted or strengthened simultaneously across all major geographies. As frameworks formalize methane monitoring, expand facility coverage, and add pollutant parameters, CEMS calibration gas demand follows — driven by compliance deadlines, not economic cycles. Each regulatory update translates directly into new certified gas formulations that facilities must procure to stay in operation.

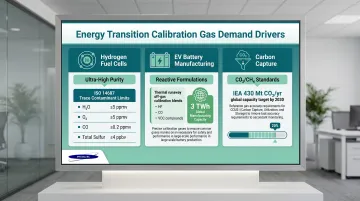

The Energy Transition Is Creating Demand for Entirely New Calibration Gas Formulations

Hydrogen fuel cell vehicles and infrastructure, EV battery manufacturing, and carbon capture projects are generating demand for gas mixture formulations that did not exist at commercial scale five years ago.

Hydrogen Fuel Cell Infrastructure

At the end of 2024, there were around 1,300 hydrogen refuelling stations (HRSs) in operation worldwide. Fuel quality for PEM fuel cells is governed by ISO 14687, which sets strict maximum concentration limits for contaminants including:

- Water (H₂O): 5 μmol/mol

- Total hydrocarbons except methane: 2 μmol/mol

- Oxygen (O₂): 5 μmol/mol

- Carbon monoxide (CO): 0.2 μmol/mol

- Total sulphur compounds: 0.004 μmol/mol

Detecting impurities at parts-per-billion (ppb) levels—such as 0.004 μmol/mol for sulfur—requires ultra-high-purity reference gases and producers capable of certifying trace-level accuracy with NIST-traceable standards.

EV Battery Manufacturing

Global battery (cell) manufacturing capacity grew almost 30% in 2024 to reach more than 3 TWh. In the US alone, manufacturing capacity doubled since 2022, reaching more than 200 GWh in 2024, with nearly 700 GWh of additional capacity under construction.

EV battery safety testing requires off-gas detection blends to monitor thermal runaway events, including mixtures containing HF, CO, and volatile organic compounds. These reactive formulations demand specialized cylinder passivation, rigorous stability management, and NIST-traceable certification—capabilities that most commodity gas suppliers lack.

Carbon Capture and Storage Expansion

As of Q1 2025, there was just over 50 million tonnes (Mt) of CO₂ capture and storage capacity in operation. Based on the current pipeline, capture capacity is set to reach around 430 Mt CO₂ per year by 2030. These projects require CO₂/CH₄ reference standards for monitoring and verification, adding another layer to energy transition calibration demand.

The Supply Challenge

Across all three of these growth areas, the production challenge is the same: commodity gas suppliers generally lack the cylinder treatment processes and documented stability data needed to deliver these formulations at shelf lives that meet field requirements. Specialty blenders that have developed proprietary passivation methods and NIST-traceable certification workflows for reactive and trace-level mixtures are the ones filling this gap.

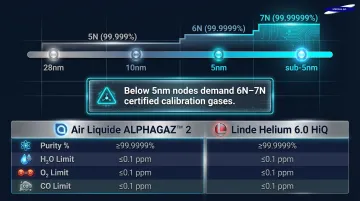

Semiconductor & Advanced Electronics Manufacturing Is Becoming a Key Calibration Gas Demand Driver

Semiconductor fabrication requires ultra-high-purity (UHP) calibration gas mixtures for process control at etching, deposition, and chamber cleaning stages, where even trace-level impurities can compromise chip yield and performance.

Historic Fab Investment Surge

Worldwide 300mm fab equipment spending is expected to increase 18% to USD 133 billion in 2026 and 14% to USD 151 billion in 2027. This growth is heavily subsidized by government initiatives:

- US CHIPS Act: USD 33.0787 billion in grant awards and up to USD 7.15 billion in loans to 35 companies across 52 projects

- EU Chips Act: Mobilizes €43 billion in public and private investment

Semiconductor Specialty Gas Market Growth

The global semiconductor specialty gas market was valued at USD 2.71 billion in 2025 and is expected to reach USD 5.34 billion by 2034, at a CAGR of 7.63%. Electronics is identified as the fastest-growing end-use industry in the gas mixtures market.

Ultra-High-Purity Requirements

Calibration and reference gases used in semiconductor environments must meet extreme purity thresholds. The table below illustrates representative specifications from established UHP suppliers:

| Supplier / Grade | Overall Purity | H₂O Limit | O₂ Limit | CO Limit |

|---|---|---|---|---|

| Air Liquide ALPHAGAZ 2 | 99.9999% (N60) | < 0.5 ppm | < 0.5 ppm | < 0.1 ppm |

| Linde Helium 6.0 HiQ | ≥ 99.9999% | ≤ 0.5 ppm | ≤ 0.5 ppm | N/A |

These specifications reflect current baseline requirements. As semiconductor nodes shrink below 5nm, demand for 6N (99.9999%) and 7N (99.99999%) calibration gases will climb steeply.

Why This Segment Favors Specialty Suppliers

Meeting UHP requirements demands more than sourcing high-purity base gases. Semiconductor customers also require:

- Multi-component formulations blended to exact PPM/PPB tolerances

- Contamination-free certification with documented traceability

- Gravimetric blending precision and rigorous analytical QC

- Long-term supply consistency across production batches

Generalist industrial gas distributors rarely maintain these capabilities. Specialty blenders with proprietary cylinder treatment processes and NIST-traceable production standards are better positioned to serve this segment reliably.

Multi-Gas Safety Monitoring Growth Is Driving Reactive and Specialty Blend Adoption

The industry-wide shift to connected, multi-gas detectors capable of simultaneously monitoring H₂S, CO, combustible gases at LEL, and O₂ is replacing simpler single-gas bump test cylinders with complex multi-component calibration mixtures.

Portable Detector Market Growth:

The portable gas detector market was estimated at USD 2.8 billion in 2025 and is expected to grow to USD 5.2 billion in 2035 at a CAGR of 6.4%. Multi-gas portable detectors dominate this space, accounting for around USD 1.8 billion in 2025.

Regulatory Enforcement Driving Compliance:

In FY 2024, OSHA conducted 34,625 inspections. OSHA and the International Safety Equipment Association (ISEA) state that "A bump test or calibration check of portable gas monitors should be conducted before each day's use in accordance with the manufacturer's instructions". If calibration-check results are not within the acceptable range, the operator must perform a full calibration.

Reactive Gas Stability Challenges:

Each multi-gas detector requires a single cylinder containing all target components at certified concentrations, raising the technical bar for the calibration gas required. Reactive gas components (H₂S, NO, NO₂, SO₂, NH₃) present significant blending and long-term stability challenges — they degrade through reaction with moisture, oxygen, or the cylinder wall itself unless specialized surface treatment and passivation processes are applied.

Not all calibration gas suppliers can reliably handle these mixtures. Specialty blenders with proprietary cylinder treatment processes and documented stability guarantees offer capabilities that generalist suppliers cannot consistently replicate:

- Produce NIST-traceable reactive blends with verified, consistent composition

- Apply internal cylinder treatment to prevent degradation at the wall surface

- Offer formal stability guarantees covering difficult mixtures like formaldehyde and nitric oxide

- Deliver longer shelf life without reformulation between deliveries

SpecGas Inc. developed its proprietary internal cylinder treatment process through decades of specialty gas R&D, tracing back to founder Alfred Boehm's research work beginning in 1976. That depth of process knowledge is what enables stable reactive blends at concentrations from PPB to percent levels.

What's Driving These Calibration Gas Market Trends — and How They're Reshaping the Industry

Regulatory & Compliance Pressure

Non-discretionary calibration requirements embedded in environmental and safety law create a demand floor that is largely recession-resilient. Procurement behavior is shifting from reactive, spot-purchase models to long-term certified supply agreements, particularly among CEMS operators and semiconductor fabs with zero tolerance for out-of-specification instrumentation.

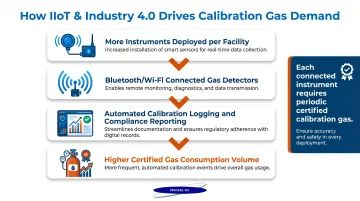

Technology Advances & Industrial Automation

IIoT integration and Industry 4.0 adoption are increasing the number of process analytical instruments deployed per facility, each requiring periodic calibration. Automated calibration logging in connected safety systems is also driving higher compliance rates and more frequent certified gas consumption.

The integration of wireless technologies (Bluetooth, Wi-Fi) and IoT capabilities into gas detectors enables real-time data transmission to centralized monitoring systems, supporting predictive maintenance and compliance reporting. This expanded connected instrument base directly increases the total volume of calibration gas required to keep it in spec.

Supply-Side Bifurcation & Competitive Dynamics

The market is bifurcating. Large commodity volumes—standard NIST-air, zero gas, simple binary blends—are served efficiently by global majors such as Linde, Air Liquide, and Air Products. Complex reactive mixtures, custom multi-component blends, and UHP formulations are increasingly sourced from specialized mid-size blenders who offer faster lead times, proprietary technical processes, and flexibility for non-standard specifications.

ISO 17034 Accreditation Barriers:

Production of Certified Reference Materials (CRMs) is governed by ISO 17034:2016, which specifies general requirements for the competence and consistent operation of reference material producers. According to ILAC, over 320 reference material producers were accredited by the ILAC MRA Signatories in 2024. Achieving this accreditation is a significant barrier to entry, ensuring that only highly competent producers can supply the market.

Cost & Logistics Constraints

Three overlapping constraints are tightening supply for specialized blends and concentrating pricing power among capable producers:

- Certification barriers — ISO 17034 accreditation requirements limit the number of qualified CRM producers

- Reactive gas handling regulations — specialized handling rules add cost and complexity for blenders of toxic and corrosive mixtures

- High-pressure cylinder transport rules — DOT and IATA restrictions increase logistics costs and limit shipping flexibility

Together, these factors create real supply concentration risk for buyers who rely on single-source procurement.

Geopolitical Supply Chain Risks:

A 2026 report noted that Q1 2026 saw a "sharp escalation in geopolitical risk following the outbreak of conflict involving Iran, compounding already fragile industrial gas supply chains". Industrial gas markets are no longer defined purely by supply-demand balance, but by geopolitical optionality and resilience. For specialty gas buyers, that means vetting not just price but a supplier's lead time track record, technical depth, and ability to maintain supply through disruption.

Future Signals for the Calibration Gas Mixture Market in 2026 and Beyond

The most critical near-term development to monitor (2026–2028) is the formalization of regulatory calibration standards for hydrogen fuel cell and EV battery safety applications. As these industries scale from R&D volumes to full commercial production, regulatory agencies will codify mandatory calibration protocols, triggering a sharp jump in certified mixture demand. Suppliers who establish technical capabilities for these formulations early—especially those with proprietary cylinder passivation processes for reactive and hydrogen-containing mixtures—will be positioned as preferred vendors when volume contracts come online.

The proliferation of low-cost ambient air quality sensor networks does not displace certified calibration gas demand. Rather, sensor expansion increases the need for reference-grade calibration at anchor monitoring stations used to validate sensor networks—meaning the growth in sensor deployment is a net positive for the certified calibration gas market.

Strategic Outlook:

Geopolitical supply chain fragmentation, trade policy shifts, and raw gas supply concentration are pushing industrial buyers toward supply reliability and domestic sourcing. Organizations best positioned for compliance and instrument accuracy are those working with certified specialty blenders that offer:

- NIST-traceable quality standards across concentration levels

- Proprietary formulation capabilities, including internal cylinder treatment for reactive gases

- Consistently fast lead times that hold regardless of broader market conditions

- The technical depth to scale into emerging applications as regulations evolve

The core advantage of choosing a technically deep supplier over a commodity provider is stability across the board — mixture stability, supply chain reliability, and the formulation flexibility to serve emerging applications that commodity suppliers cannot or will not handle profitably.

Frequently Asked Questions

What is the mix for calibration gas?

Calibration gas compositions vary entirely by application. Common examples include CO in nitrogen for CO detector calibration, multi-component NOx/SO₂/CO blends for CEMS, and H₂ in nitrogen for fuel cell testing. The composition is dictated by the specific instrument being calibrated and the regulatory standard it must meet.

Is 2.5% methane 50% LEL?

Yes, methane's lower explosive limit (LEL) is approximately 5% by volume in air, making 2.5% methane equal to 50% LEL. This is a common calibration concentration for combustible gas detectors. Manufacturing this mixture requires strict safety protocols to prevent ignition risk during blending.

What is driving growth in the calibration gas mixture market in 2026?

Three factors are pushing demand upward:

- Expanding CEMS mandates under environmental regulations

- New formulation needs from hydrogen and EV energy transition applications

- Accelerating semiconductor fab investment requiring ultra-high-purity mixtures

Which industries use the most calibration gas mixtures?

Environmental monitoring is the largest segment at ~30% of demand, followed by industrial process control (~25%), automotive and transportation testing (~20%), laboratory and analytical applications (~15%), and occupational health and safety (~10%).

What does NIST traceable mean for calibration gas?

NIST traceability means the calibration gas mixture's certified concentration has been verified using measurement processes linked to the National Institute of Standards and Technology. This ensures documented accuracy that satisfies regulatory requirements for instrument validation under ISO, OSHA, and other regulatory programs.

How is the energy transition affecting calibration gas demand?

Hydrogen fuel cell validation, EV battery off-gas safety testing, and carbon capture monitoring are all generating demand for new formulations. Many involve reactive or exotic components—such as HF-bearing blends—requiring specialized blending capabilities, proprietary cylinder passivation, and stability guarantees that most commodity suppliers cannot provide.