For procurement managers, lab directors, and R&D professionals, understanding where supply, pricing, and availability are heading in 2026 and beyond isn't optional—it's strategic. Semiconductor fabs expanding under the CHIPS Act, university research labs conducting trace-level analytical work, and emissions monitoring operations all depend on reliable access to certified-purity hydrogen. As industrial demand surges and clean energy investments reshape production infrastructure, precision buyers face a tightening market where supplier choice, traceability standards, and lead times will determine operational continuity.

This article examines the high purity hydrogen market's size and growth trajectory through 2026, the mega-forces driving demand, segmentation by purity grade and application, regional dynamics, and what these shifts mean for specialty buyers who cannot afford supply disruptions.

Key Takeaways

- High purity hydrogen (≥99.9%) is a fast-growing specialty segment — demand is accelerating across electronics, semiconductors, pharmaceuticals, and clean energy

- The global market reached $3.72 billion in 2026 and is projected to hit $6.37 billion by 2035, growing at a 6.16% CAGR

- Three forces drive growth: the energy transition, $640B+ in U.S. semiconductor investments since 2020, and the DOE's $7 billion hydrogen hub initiative

- Three purity tiers exist (99.9–99.99%, 99.99–99.999%, >99.999%), with ultra-high purity grades commanding premium prices for semiconductor and analytical use

- Labs sourcing high purity hydrogen should verify NIST-traceable standards and supplier reliability before supply constraints tighten further

What Is High Purity Hydrogen? Understanding the Purity Tiers

High purity hydrogen refers to hydrogen gas with a purity level of 99.9% or higher. This designation covers multiple distinct grades, each suited to specific industrial or scientific applications where even trace contaminants can compromise results, damage equipment, or reduce product yield.

Purity Grade Breakdown

The commercial market recognizes three primary purity tiers:

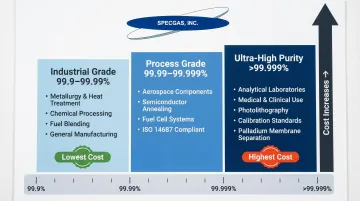

99.9–99.99% — Industrial Grade:

- Used in general industrial processes and chemical applications

- Suitable for metallurgical processes where hydrogen acts as a reducing agent

- Appropriate for some power generation and fuel blending applications

- Lowest cost tier, produced through standard purification methods

99.99–99.999% — Process Grade:

- Required for aerospace applications and advanced manufacturing

- Used in semiconductor fabrication processes including annealing and cleaning

- Mandated for many fuel cell applications per ISO 14687:2019 standards

- Moderate cost tier requiring additional purification steps

>99.999% — Ultra-High Purity (UHP):

- Essential for research laboratories and analytical instrumentation

- Required for medical applications where contamination risks are unacceptable

- Critical for photolithography in semiconductor manufacturing at sub-7nm nodes

- Necessary for calibration gas standards requiring NIST traceability

- Highest cost tier, demanding advanced purification technologies like palladium membrane separation

According to the EIA's 2018 Manufacturing Energy Consumption Survey, electronics manufacturers paid an average of $86.19 per MMBtu for hydrogen—more than 13 times higher than the $6.18/MMBtu paid by chemical producers and $6.77/MMBtu paid by refiners. That price gap reflects the cost of the additional purification steps, certified analysis, and traceability documentation that precision applications require.

High purity hydrogen differs fundamentally from industrial-grade hydrogen. Industrial hydrogen is typically produced as a byproduct or via steam methane reforming (SMR) for bulk refining and chemical use, with purity as a secondary concern.

Achieving high purity grades requires additional processing steps — pressure swing adsorption (PSA), cryogenic distillation, or palladium diffusion — along with certified analytical verification. For calibration and research applications, documented traceability to NIST reference standards is also required.

High Purity Hydrogen Market Size and Growth Forecast for 2026

The global high purity hydrogen market reached $3.72 billion in 2026 and is projected to grow to $6.37 billion by 2035, representing a compound annual growth rate (CAGR) of 6.16% during the forecast period. Growth is driven by expanding demand from semiconductor manufacturing, fuel cell power generation, and laboratory research applications.

The United States leads as one of the largest and most active markets globally, benefiting from:

- Advanced industrial infrastructure for gas production and distribution

- Significant government investment through the Inflation Reduction Act

- The DOE's $7 billion hydrogen hub program selected in October 2023

- Rapidly expanding fuel cell and semiconductor sectors

That industrial foundation translates directly into production scale. Total U.S. hydrogen production reached 10 million metric tons in 2018, with approximately 40% classified as merchant hydrogen sold by industrial gas companies. Exact figures for the high-purity segment aren't broken out separately, but the share destined for high-purity applications is growing as industries shift toward cleaner, more precise processes. By 2024, global demand for high-purity hydrogen exceeded 95 million metric tons.

Market sizing is complicated because "high purity hydrogen" spans both large-volume industrial uses (refining, chemical production) and small-volume precision uses (calibration gases, laboratory standards). For labs, semiconductor plants, and monitoring equipment operators, the precision/specialty segment is the relevant market — one where **purity certification and NIST traceability** drive value as much as volume does.

Key Growth Drivers Fueling the High Purity Hydrogen Market

The Clean Energy Transition and Fuel Cell Expansion

Global decarbonization commitments represent the single largest structural driver of hydrogen demand growth. Heavy industry, transportation, and power generation are all looking to hydrogen as a clean fuel or feedstock, creating new demand streams across multiple sectors:

- Fuel cell vehicles for automotive and commercial transportation

- Stationary fuel cells for data centers, hospitals, and distributed power Hydrogen blending in gas turbines for power generation

- Green hydrogen as industrial feedstock replacing fossil-derived hydrogen

The IEA Net Zero Emissions by 2050 Scenario projects total global hydrogen demand reaching 150 million tonnes by 2030 and 430 million tonnes by 2050. Fuel cell technology is scaling rapidly to meet that demand: the global proton exchange membrane fuel cell (PEMFC) market was estimated at $5.68 billion in 2025 and is projected to reach $27.23 billion by 2033, growing at a 22.4% CAGR.

Purity standards matter critically for fuel cell hydrogen. ISO 14687 Grade D requires a minimum hydrogen fuel index of 99.97% and mandates strict maximum contaminant limits, including carbon monoxide ≤0.2 μmol/mol and total sulfur compounds ≤0.004 μmol/mol. These specifications directly drive demand for high-purity production and distribution infrastructure.

Semiconductor and Electronics Manufacturing Demand

Semiconductor and electronics manufacturing is one of the highest-value demand segments for ultra-high purity hydrogen. The gas is essential for:

- Chemical vapor deposition (CVD) processes

- Epitaxial growth of thin films

- Annealing processes that improve crystal structure

- Surface cleaning of wafers between processing steps

- Extreme ultraviolet (EUV) lithography for sub-7nm node fabrication

Even parts-per-billion-level impurities can damage wafers, reduce yield, or compromise product quality — which is why purity requirements in this sector are among the most demanding in any industry.

The CHIPS Act has catalyzed unprecedented semiconductor fab expansion: since 2020, companies have announced over 140 projects across 30 states, totaling more than $640 billion in private investments. That buildout translates directly into rising UHP hydrogen demand. The high purity gas market for electronics (which includes UHP hydrogen) is projected to grow from $37.46 billion in 2025 to $52.78 billion by 2030, registering a 7.1% CAGR.

Government Policy and Infrastructure Investment

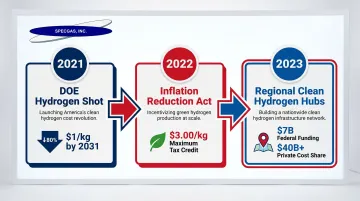

U.S. policy milestones are reshaping hydrogen economics and availability:

- DOE Hydrogen Shot (2021) — Targets an 80% cost reduction to $1/kg by 2031, putting clean hydrogen on par with conventional fuels.

- Inflation Reduction Act (2022) — Offers a maximum credit of $3.00 per kilogram for clean hydrogen produced with lifecycle GHG emissions below 0.45 kg CO₂e per kg H₂, sustained over 10 years.

- Regional Clean Hydrogen Hubs (October 2023) — The DOE awarded $7 billion in federal funding, leveraging over $40 billion in private cost share. Pennsylvania participates in two hubs — ARCH2 and MACH2 — the only state to do so.

Similar policies across Europe and Asia-Pacific are driving synchronized global demand. The EU REPowerEU Strategy set targets of producing and importing 10 million tonnes each of renewable hydrogen by 2030. Germany's updated National Hydrogen Strategy doubled its domestic electrolyzer target from 5 GW to at least 10 GW by 2030.

Market Challenges and Barriers

Three interconnected barriers slow high purity hydrogen market growth: production costs, distribution infrastructure, and the unresolved tension between sustainability mandates and supply chain reality.

Production Cost Premium

Achieving purity levels above 99.999% requires additional purification steps beyond standard SMR or electrolysis. The modeled levelized cost of clean hydrogen produced from renewable electricity using current PEM electrolyzer technology is approximately $5 to $7 per kilogram (2022 dollars, without subsidies) — significantly higher than fossil-based production. EIA MECS data puts the cost gap in stark terms: electronics buyers pay 13x more per energy unit than chemical buyers, reflecting the purification premium built into every UHP cylinder.

Infrastructure and Supply Chain Gaps

Cost is only part of the problem. Hydrogen distribution networks — pipelines, compression, storage — remain underdeveloped across most regions, limiting reliable delivery of certified-purity product to end users. For precision applications, the consequences are immediate:

- Supply chain disruptions can halt calibration gas programs and research lab operations entirely

- Geographic concentration of production capacity leaves buyers exposed without diversified supplier relationships

- Certified-purity verification requirements add lead time that standard industrial gas logistics don't accommodate

The Green Hydrogen Transition Challenge

Sustainability pressure compounds the distribution problem. In 2023, around two-thirds of dedicated hydrogen production relied on natural gas and approximately 20% on coal — while low-emissions hydrogen represented less than 1% of total output. As buyers, particularly in Europe, increasingly require green hydrogen credentials under sustainability regulations, producers must scale electrolysis cost-effectively without sacrificing purity standards. That's not a solved problem. For precision applications requiring NIST-traceable gas standards, sourcing green hydrogen that meets both environmental and analytical specifications requires separate vendor relationships and certification chains that don't yet exist at scale.

Market Segmentation: By Purity Grade, Application, and Region

Segmentation by Purity Grade

The three purity tiers serve distinct markets with different growth trajectories:

- 99.9–99.99% purity segment dominates with approximately 45% market share, driven by industrial refining and chemical applications

- 99.99–99.999% purity grade is the fastest-growing tier by demand, accounting for over 50% of incremental growth, fueled by aerospace and fuel cell expansion

- >99.999% segment accounted for nearly 40% of total consumption in 2024 due to high-precision electronics demand

The highest-purity tier is the smallest by volume but the fastest-growing and highest-margin segment, driven by analytical, semiconductor, and medical demand.

Segmentation by Application

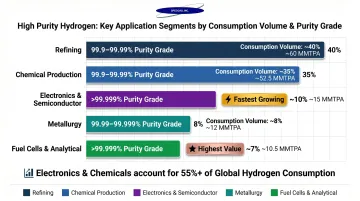

Electronics and chemicals collectively accounted for more than 55% of global high purity hydrogen consumption in 2024. Five major application segments drive this demand:

- Refining — Historically the largest consumer by volume; uses hydrogen for hydrocracking and desulfurization at 99.9–99.99% purity

- Chemical Production — Ammonia and methanol synthesis rely on substantial hydrogen volumes, with increasing demand for certified purity in quality control

- Electronics & Semiconductor Manufacturing — The fastest-growing segment, requiring >99.999% purity for CVD, etching, and lithography where trace impurities directly compromise yield

- Metallurgy — Hydrogen acts as a reducing agent in metal processing and heat treatment; growing volume driven by hydrogen-based direct reduction of iron

- Fuel Cells, Aerospace & Analytical Uses — Small by volume but high-value, demanding the highest purity grades and NIST-traceable standards

Regional Market Breakdown

North America: The U.S. leads with advanced industrial infrastructure, active government investment, and semiconductor expansion. North America consumed over 2,500 kilotons of high purity hydrogen in 2024, with the U.S. contributing 2,100 kilotons. Pennsylvania's inclusion in two DOE hydrogen hubs (MACH2 and ARCH2) places the state at the center of expanding production and distribution networks — a direct advantage for Pennsylvania-based suppliers like SpecGas, located in Bridgeport, PA.

Asia-Pacific: Leads globally with approximately 45% market share, consuming over 4,500 kilotons in 2024. China dominates by volume for chemical and refining uses. Japan and South Korea lead in fuel cell and mobility applications, with stringent purity standards driving UHP demand. Taiwan's semiconductor industry represents a critical high-purity consumption center.

Europe: Consumed approximately 3,000 kilotons in 2024. Germany leads with aggressive green hydrogen investment tied to its Energiewende policy goals. The EU's raised hydrogen supply targets under REPowerEU are driving infrastructure development and production capacity expansion. The Middle East is emerging as a potential low-cost producer eyeing export markets.

What This Market Growth Means for Buyers and Laboratories

As demand for high purity hydrogen grows from large industrial players—refiners, semiconductor fabs, automotive fuel cell manufacturers—specialty precision buyers face practical supply implications. Research labs, calibration gas users, university labs, and emissions monitoring operations may encounter:

- Longer lead times as large commodity suppliers prioritize volume customers

- Greater price volatility tied to industrial demand cycles

- Allocation constraints during supply disruptions or infrastructure bottlenecks

- Quality variability from suppliers lacking precision gas expertise

This makes supplier choice, reliability, and lead time critical factors in procurement strategy. What should buyers look for in a high purity hydrogen supplier for precision applications?

Key supplier selection criteria:

- NIST traceability of gas standards with documented certification chains

- Certified analytical documentation including Certificates of Analysis with concentration, uncertainty, and expiration data

- Consistent purity verification through regular testing against NIST Standard Reference Materials

- Ability to produce small-volume or custom blends tailored to specific applications

- Fast turnaround for both standard and rush orders

For labs that can't absorb supply disruptions, these criteria narrow the field considerably. SpecGas Inc., a Bridgeport, PA specialty gas blender founded in 2001, provides NIST-traceable high purity hydrogen and precision blends with faster lead times than most commodity suppliers—including rush service. Where large suppliers allocate capacity toward volume accounts, SpecGas focuses on custom blends for labs and manufacturers where a missed shipment means halted operations.

Purity certification is only part of the picture. For reactive gas mixtures and trace-level calibration standards, the shelf life and concentration stability of the gas in the cylinder matter just as much. SpecGas's proprietary cylinder treatment process extends shelf life and ensures consistency over time—a capability most commodity suppliers don't offer for specialty applications. That stability is especially valuable for university research labs running long-term experiments and calibration facilities that depend on instrument uptime.

Frequently Asked Questions

Can you buy compressed high-purity hydrogen?

Yes, compressed high-purity hydrogen is commercially available from specialty gas suppliers and industrial gas companies in various cylinder sizes and purity grades. For precision applications requiring NIST traceability or certified calibration-grade hydrogen, specialty gas suppliers like SpecGas are the appropriate source.

What purity level is considered "high purity" hydrogen?

High purity hydrogen typically refers to hydrogen with a purity of 99.9% or greater. Ultra-high purity (UHP) grade starts at 99.999% and above. Different applications require different tiers: semiconductor and analytical uses demand the highest grades, while industrial processes may use lower-purity specifications.

What industries use the most high purity hydrogen?

The top consuming sectors include:

- Petroleum refining (largest by volume)

- Chemical manufacturing (ammonia, methanol production)

- Electronics and semiconductor fabrication (highest purity requirements)

- Metallurgy (hydrogen as a reducing agent)

- Clean energy and fuel cell applications

Electronics buyers pay significantly more per unit due to stringent purity specifications.

What is driving growth in the high purity hydrogen market?

Main drivers include the global clean energy transition, expansion of semiconductor manufacturing (over $640 billion in U.S. investments since 2020), government hydrogen infrastructure investment including DOE hydrogen hubs and IRA tax credits, and rising demand in fuel cell vehicles and stationary power applications.

How is high purity hydrogen produced?

Industrial production methods — steam methane reforming (SMR) or electrolysis — provide the base hydrogen. Additional purification steps such as pressure swing adsorption, palladium diffusion, or cryogenic distillation then achieve certified purity levels. Green hydrogen via electrolysis powered by renewables is an increasingly prominent clean production route.

What is the difference between high purity hydrogen and industrial hydrogen?

Industrial hydrogen is produced in bulk for refining and chemical processes where exact purity is less critical. High purity hydrogen undergoes additional purification and analytical verification, and certified grades carry documentation — including Certificates of Analysis and NIST traceability — required by labs and semiconductor fabs.